Federal Budget 2021 – 2022

PERSONAL TAXATION

Personal tax rates unchanged for 2021–2022

In the Budget, the Government did not announce any personal tax rates changes, having already brought forward the Stage 2 tax rates to 1 July 2020 in the October 2020 Budget. The Stage 3 tax changes will commence from 1 July 2024, as previously legislated.

The 2021–2022 tax rates and income thresholds for residents are therefore unchanged from 2020–2021:

- taxable income up to $18,200 – nil;

- taxable income of $18,201 to $45,000 – 19% of excess over $18,200;

- taxable income of $45,001 to $120,000 – $5,092 plus 32.5% of excess over $45,000;

- taxable income of $120,001 to $180,000 – $29,467 plus 37% of excess over $120,000; and

- taxable income of more than $180,001 – $51,667 plus 45% of excess over $180,000.

Stage 3: from 2024–2025

The Stage 3 tax changes will commence from 1 July 2024, as previously legislated. From 1 July 2024, the 32.5% marginal tax rate will be cut to 30% for one big tax bracket between $45,000 and $200,000. This will more closely align the middle tax bracket of the personal income tax system with corporate tax rates. The 37% tax bracket will be entirely abolished at this time.

Therefore, from 1 July 2024, there will only be three personal income tax rates: 19%, 30% and 45%. From 1 July 2024, taxpayers earning between $45,000 and $200,000 will face a marginal tax rate of 30%. With these changes, around 94% of Australian taxpayers are projected to face a marginal tax rate of 30% or less.

Low income offsets: LMITO and LITO retained for 2021–2022L

Low and middle income tax offset

The Government also announced in the Budget that the low and middle income tax offset (LMITO) will continue to apply for the 2021–2022 income year. The LMITO was otherwise legislated to only apply until the end of the 2020–2021 income year, meaning low-to-middle income earners would have seen lower tax refunds in 2022.

The amount of the LMITO is $255 for taxpayers with a taxable income of $37,000 or less. Between $37,000 and $48,000, the value of LMITO increases at a rate of 7.5 cents per dollar to the maximum amount of $1,080. Taxpayers with taxable incomes from $48,000 to $90,000 are eligible for the maximum LMITO of $1,080. From $90,001 to $126,000, LMITO phases out at a rate of 3 cents per dollar.

Consistent with current arrangements, the LMITO will be received on assessment after individuals lodge their tax returns for the 2021–22 income year.

Low income tax offset

The low income tax offset (LITO) will also continue to apply for the 2021–2022 income year. The LITO was intended to replace the former low income and low and middle income tax offsets from 2022–2023, but the new LITO was brought forward in the 2020 Budget to apply from the 2020–2021 income year.

The maximum amount of the LITO is $700. The LITO will be withdrawn at a rate of 5 cents per dollar between taxable incomes of $37,500 and $45,000, and then at a rate of 1.5 cents per dollar between taxable incomes of $45,000 and $66,667.

Self-education expenses: $250 threshold to be removed

The Government will remove the exclusion of the first $250 of deductions for prescribed courses of education. The first $250 of a prescribed course of education expense is currently not deductible.

Primary 183-day test for individual tax residency

The Government will replace the existing tests for the tax residency of individuals with a primary “bright line” test under which a person who is physically present in Australia for 183 days or more in any income year will be an Australian tax resident.

People who do not meet the primary test will be subject to secondary tests that depend on a combination of physical presence and measurable, objective criteria.

Child care subsidies to change 1 July 2022

The Budget confirmed that the Government will make an additional $1.7 billion investment in child care. The changes will commence on 1 July 2022 (that is, not in the next financial year). This measure was previously announced on 2 May 2021.

Commencing on 1 July 2022, the Government will:

- increase the child care subsidies available to families with more than one child aged 5 and under in child care by adding an additional 30 percentage point subsidy for every second and third child (stated to benefit around 250,000 families); and

- remove the $10,560 cap on the Child Care Subsidy (which the Government expects to benefit around 18,000 families).

BUSINESS TAXATION

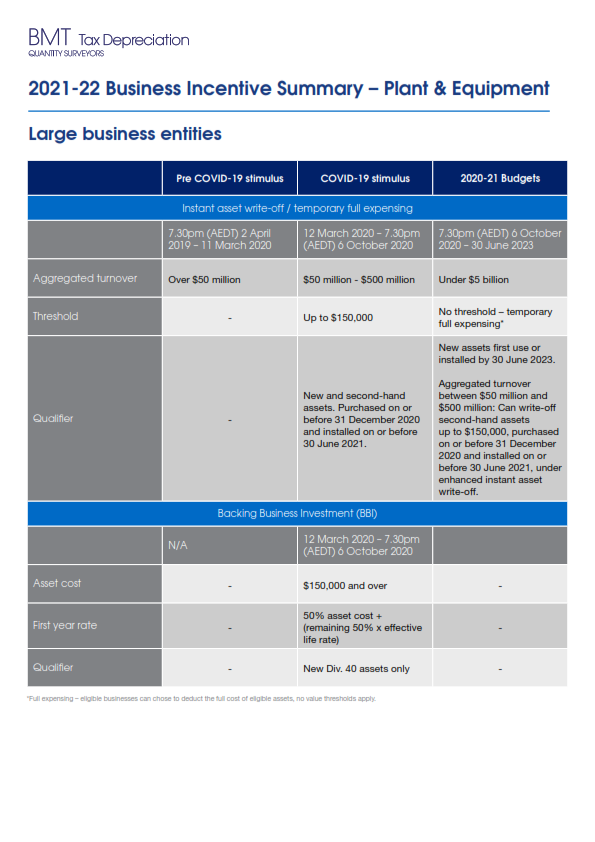

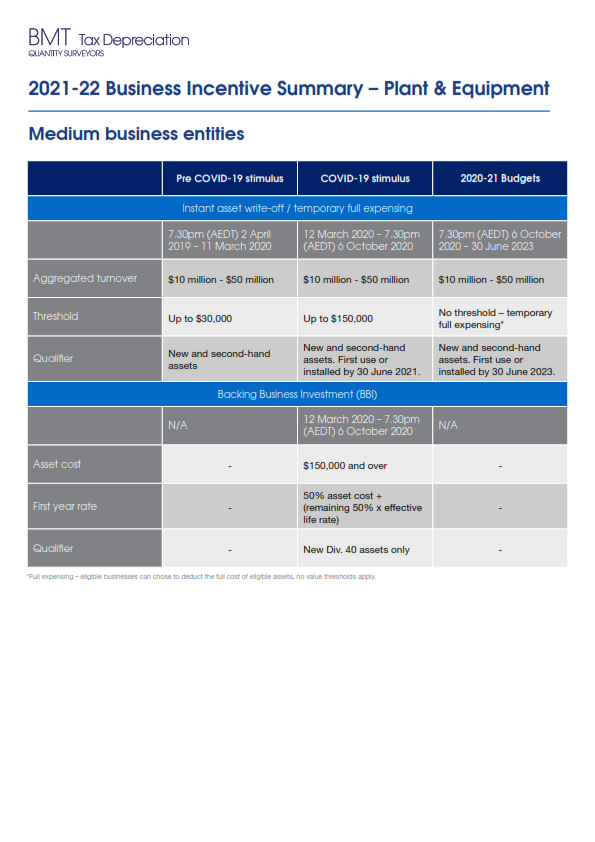

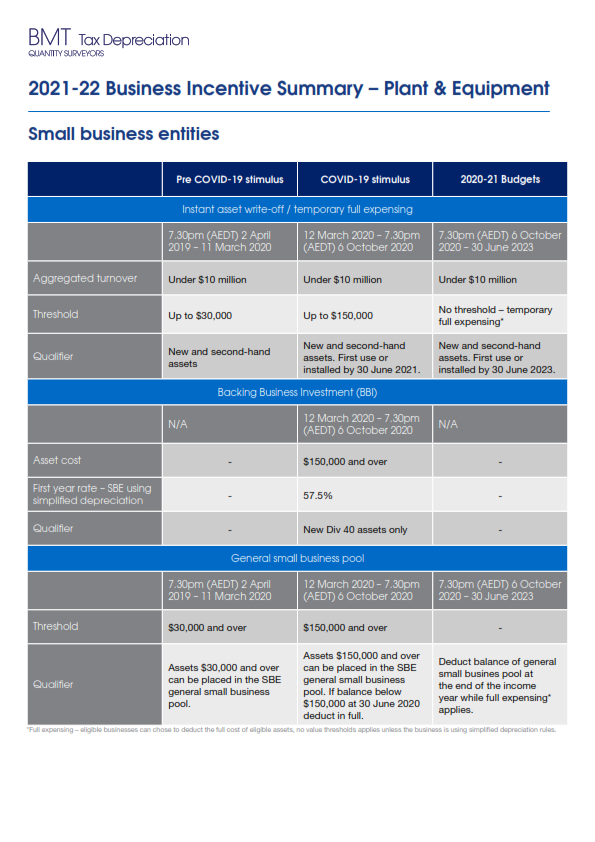

Temporary full expensing: extended to 30 June 2023

The Government will extend the temporary full expensing measure until 30 June 2023. It was otherwise due to finish on 30 June 2022.

Other than the extended date, all other elements of temporary full expensing will remain unchanged.

Currently, temporary full expensing allows eligible businesses to deduct the full cost of eligible depreciating assets, as well as the full amount of the second element of cost. A business qualifies for temporary full expensing if it is a small business (annual aggregated turnover under $10 million) or has an annual aggregated turnover under $5 billion. Annual aggregated turnover is generally worked out on the same basis as for small businesses, except that the threshold is $5 billion instead of $10 million.

There is an alternative test, so a corporate tax entity qualifies for temporary full expensing if:

- its total ordinary and statutory income, other than non-assessable non-exempt income, is less than $5 billion for either the 2018–2019 or the 2019–2020 income year (some additional conditions apply for entities with substituted accounting periods); and

- the total cost of certain depreciating assets first held and used, or first installed ready for use, for a taxable purpose in the 2016–2017, 2017–2018 and 2018–2019 income years (combined) exceeds $100 million.

Loss carry-back extended by one year

Under the temporary, COVID-driven restoration of the loss carry-back provisions announced in the previous Budget, an eligible company (aggregated annual turnover of up to $5 billion) could carry back a tax loss for the 2019–2020, 2020–2021 or 2021–2022 income years to offset tax paid in the 2018–2019 or later income years.

The Government has announced it will extend this to include the 2022–2023 income year. Tax refunds resulting from loss carry-back will be available to companies when they lodge their 2020–2021, 2021–2022 and now 2022–2023 tax returns.

Employee share schemes: cessation of employment removed as a taxing point

The Government will remove the cessation of employment as a taxing point for tax-deferred employee share schemes (ESSs). There are also other changes designed to cut “red tape” for certain employers.

Cessation of employment change

Currently, under a tax-deferred ESS and where certain criteria are met, employees may defer tax until a later tax year (the deferred taxing point). In such cases, the deferred taxing point is the earliest of:

- cessation of employment;

- in the case of shares, when there is no risk of forfeiture and no restrictions on disposal;

- in the case of options, when the employee exercises the option and there is no risk of forfeiting the resulting share and no restriction on disposal; and

- the maximum period of deferral of 15 years.

The change announced in the latest Budget will result in tax being deferred until the earliest of the remaining taxing points.

TAX COMPLIANCE AND INTEGRITY

Allowing small businesses to pause disputed ATO debt recovery

The Government will introduce legislation to allow small businesses to pause or modify ATO debt recovery action where the debt is being disputed in the Administrative Appeals Tribunal (AAT). Treasurer Josh Frydenberg had earlier announced this measure on 8 May 2021.

Specifically, the changes will allow the Small Business Taxation Division of the AAT to pause or modify any ATO debt recovery actions – such as garnishee notices and the recovery of general interest charge (GIC) or related penalties – until the underlying dispute is resolved by the AAT. This measure is intended to provide an avenue for small businesses to ensure they are not required to start paying a disputed debt until the matter has been determined by the AAT.

SUPERANNUATION

Superannuation contributions work test to be repealed from 1 July 2022

The superannuation contributions work test exemption will be repealed for voluntary non-concessional and salary sacrificed contributions for those aged 67 to 74 from 1 July 2022.

As a result, individuals under age 75 will be allowed to make or receive non-concessional (including under the bring-forward rule) or salary sacrifice contributions from 1 July 2022 without meeting the work test, subject to existing contribution caps. However, individuals aged 67 to 74 years will still have to meet the work test to make personal deductible contributions.

Currently, individuals aged 67 to 74 years can only make voluntary contributions (both concessional and non-concessional), or receive contributions from their spouse, if they work at least 40 hours in any 30-day period in the financial year in which the contributions are made (the “work test”). The work test age threshold previously increased from 65 to 67 from 1 July 2020 as part of the 2019–2020 Budget.

Non-concessional contributions and bring-forward

The Government confirmed that individuals under age 75 will be able to access the non-concessional bring forward arrangement (ie three times the annual non-concessional cap over three years), subject to meeting the relevant eligibility criteria. However, we note that the Government is still yet to legislate its 2019–2020 Budget proposal to extend the bring-forward age limit so that anyone under age 67 can access the bring-forward rule from 1 July 2020. The proposed legislation for the 2019–2020 Budget measure is yet to be passed by the Senate.

The Government also noted that the existing restriction on non-concessional contributions will continue to apply for people with total superannuation balances above $1.6 million ($1.7 million from 2021–2022).

Downsizer contributions eligibility age reduced to 60

The minimum eligibility age to make downsizer contributions into superannuation will be lowered to age 60 (down from age 65) from 1 July 2022.

The proposed reduction in the eligibility age will mean that individuals aged 60 or over can make an additional non-concessional contribution of up to $300,000 from the proceeds of selling their home. Either the individual or their spouse must have owned the home for 10 years.

The maximum downsizer contribution is $300,000 per contributor ($600,000 for a couple), although the entire contribution must come from the capital proceeds of the sale price. As under the current rules, a downsizer contribution must be made within 90 days after the home changes ownership (generally the date of settlement).

Downsizer contributions are an important consideration for senior Australians nearing retirement as they do not count towards an individual’s non-concessional contributions cap and are exempt from the contribution rules. They are also exempt from the restrictions on non-concessional contributions for people with total superannuation balances above $1.6 million ($1.7 million from 2021–2022). People with balances over the transfer balance cap ($1.7 million from 2021–2022) can also a make a downsizer contribution; however, the downsizer amount will count towards that cap when savings are converted to the retirement phase.

First Home Super Scheme to be extended for withdrawals up to $50,000

The Budget confirmed that the maximum amount of voluntary superannuation contributions that can be released under the First Home Super Saver (FHSS) scheme will be increased from $30,000 to $50,000. The Treasurer previously announced this measure on 8 May 2021.